Take advantage of the benefits of strategic, active asset allocation.

“Don’t put all your eggs in one basket.” That’s common advice for investors, and for good reason. Spreading assets across different baskets – such as stocks and bonds – can help to lower risk if one or more baskets hit a rough patch in the markets. This type of diversification can get quite sophisticated, breaking down the big asset baskets into smaller ones such as small-cap, large-cap, Canadian, U.S. and international stocks, as well as government, corporate, Canadian, U.S. and international bonds. But strategic, active asset allocation adds another important dimension. In contrast to simply diversifying a portfolio, active asset allocation moves eggs between baskets based on current opportunities in the financial markets. Whereas diversification is a relatively static approach – choosing how many eggs go into each basket and then leaving them alone – active asset allocation is dynamic. What’s most important to investors, of course, is that adjusting a portfolio’s positioning may help to reduce risk and improve returns over longer periods of time.

A closer look at asset allocation

Active asset allocation manages a portfolio’s risk and reward by continually adjusting the asset mix, that is, how much is invested in various asset classes, such as stocks, bonds and cash. These asset classes tend to be associated with different levels of risk and historical returns, and also tend to perform differently at different points in an economic cycle. The goal of asset allocation is to combine asset classes in such a way as to achieve the highest possible return with the lowest risk through various economic environments – while also remaining true to the portfolio’s stated objective. It’s a complex process, best achieved through a professionally managed asset allocation portfolio.

How it works

In practical terms, a portfolio managed according to an active asset allocation strategy might start out with the same mix of asset classes as a diversified portfolio. Over time, however, the asset mix may shift based on the portfolio manager’s evaluation of broad global economic trends, how expensive or cheap certain asset classes become, and many other factors.

An asset allocation portfolio may include both actively managed mutual funds and passively managed exchange-traded funds (ETFs). Sometimes, the mutual funds make up the core of the portfolio, while ETFs allow the portfolio manager to quickly and inexpensively exploit very specific or non-traditional asset classes and shorter-term opportunities. By complementing active management with passive management, asset allocation portfolios structured in this way can provide investors with another layer of diversification. It’s important to note that professionally managed asset allocation portfolios depend on a portfolio manager’s expertise. The manager is responsible for both identifying the best opportunities and assessing their potential to have a positive impact on the portfolios. This means it’s wise to research different managers and choose one with a strong track record – an area where your advisor can provide invaluable support.

Long-term benefits to investors

Asset allocation allows managers to more actively manage portfolios toward better performance and lower risk, and to harness the power of a strategy many consider to be a key determinant of longer-term investment success. Its benefits run even deeper than that, however, because asset allocation may also give investors more confidence in their investments. Secure in the knowledge that the professional managers they’ve chosen are monitoring and responding to events affecting the markets, they may be less tempted to respond to temporary dips by selling and then staying on the sidelines until markets recover. Remaining invested in the markets helps investors avoid selling low (after a dip) and buying high (after a recovery). In this way, asset allocation can reinforce the investing discipline many advisors advocate, helping investors stay focused on their short-term and long-term financial goals because they know managers with deep experience are carefully watching market conditions and making any necessary portfolio adjustments.

Determine if asset allocation is right for you

Talk to your advisor about whether strategic, active asset allocation can help you achieve your objectives. Whether it’s appropriate for you will depend on factors such as your investment goals, tolerance for risk and time before you need access to your money. It’s an approach that may deepen the advantages of diversification for you, enhancing your investment portfolio’s potential for reward and protection from risk.

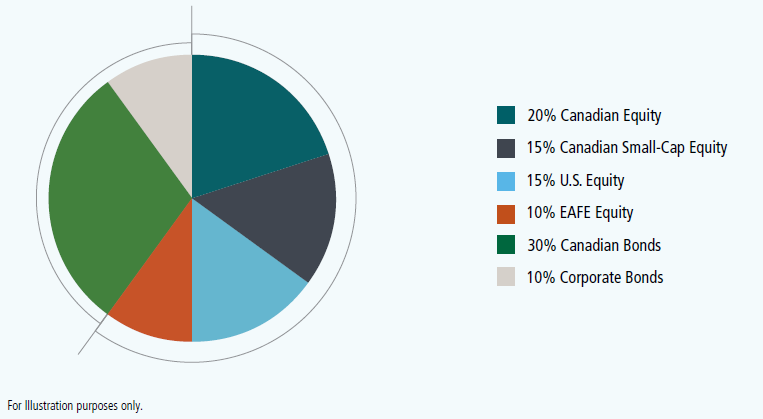

DIVERSIFICATION VS. ASSET ALLOCATION

The diagrams below illustrate the difference between a diversified portfolio and a portfolio using an active asset allocation strategy.

A diversified portfolio might look like this for a fairly long period of time.

An asset allocation strategy would look more like this.

Source: Manulife Asset Management June 2017. Returns in CAD. This simulated Asset Allocation Index is represented by a Dividend Income Fund 15%, a U.S. All Cap Equity Fund 25%, a World Investment Fund 15%, an Asia Equity Class 5%, a U.S. Tactical Credit Fund 10%, a Strategic Income Fund 30%. Benchmark represented by S&P/TSX Composite TR 20%, S&P 500 TR 25%, MSCI EAFE NR 5%, MSCI AC Asia ex Japan Index 10%, Bank of America Merrill Lynch US High Yield Index 10%, Bbg Barclays Global Aggregate Bond TR 30%. It is not possible to invest directly in an index. Past performance is not a guarantee of future results. The rate of return shown is used only to illustrate the effects of the compound growth rate and is not intended to reflect future values of the asset allocation service or returns on investment from the use of the asset allocation service. For illustration purposes only.

© 2017 Manulife. The persons and situations depicted are fictional and their resemblance to anyone living or dead is purely coincidental. This media is for information purposes only and is not intended to provide specific financial, tax, legal, accounting or other advice and should not be relied upon in that regard. Many of the issues discussed will vary by province. Individuals should seek the advice of professionals to ensure that any action taken with respect to this information is appropriate to their specific situation. E & O E. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. Any amount that is allocated to a segregated fund is invested at the risk of the contractholder and may increase or decrease in value. www.manulife.ca/accessibility